Millions of Americans aged 65 and older are asking: how does the senior deduction work? Introduced in 2025 under the One Big Beautiful Bill Act, this enhanced tax deduction allows eligible seniors to reduce their taxable income by up to $6,000 per person, significantly lowering tax bills for middle-income retirees. Unlike previous senior tax breaks, this deduction is available whether you itemize or take the standard deduction, and it stacks on top of other existing benefits.

But it is not automatic. To claim it, you must be 65 or older by December 31 of the tax year, file jointly if married, and meet income thresholds. The deduction begins to phase out at $75,000 MAGI for singles and $150,000 for joint filers, disappearing entirely at $175,000 and $250,000 respectively. And it will not last forever. It expires after tax year 2028, unless Congress acts to renew it.

Eligibility Requirements for the Senior Deduction

To answer how does the senior deduction work, you first need to know if you qualify. The IRS has three main criteria: age, filing status, and income.

Age: You Must Be 65 by Year-End

You qualify if you turn 65 or older by December 31 of the tax year. It does not matter if you turn 65 on January 1 or December 31. You get the full deduction, provided other conditions are met.

Key age requirements include:

• Born on December 15, 1960? You turn 65 in 2025, so you are eligible for the 2025 tax year

• If you turn 64 during the year, you do not qualify

• No partial credit is available for younger ages

Social Security income is not required. Even if you are not collecting benefits, you can claim the deduction as long as you meet the age rule.

Filing Status: Married Couples Must File Jointly

Married taxpayers must file jointly to claim the senior deduction. If you file Married Filing Separately, you are ineligible, even if both spouses are 65 or older.

Other filing statuses are allowed:

• Single

• Head of Household

• Qualifying Widow(er)

Only one spouse needs to be 65 or older to claim the $6,000 deduction for that spouse. But if both are 65 or older, the couple can claim up to $12,000 combined.

Income Limits: MAGI Triggers Phase-Out

The deduction is not available to high earners. It phases out based on Modified Adjusted Gross Income (MAGI).

Full deduction is available up to $75,000 MAGI for single filers and $150,000 for married filing jointly. The phase-out range extends from $75,001 to $175,000 for singles and $150,001 to $250,000 for joint filers. No deduction is available once MAGI exceeds $175,000 (single) or $250,000 (joint).

For every $1 of MAGI above the threshold, the deduction is reduced by $0.06.

Calculating Your Reduced Deduction

Follow these steps to calculate your reduced deduction:

Step 1: Subtract the phase-out start from your MAGI

Step 2: Multiply the excess by 0.06

Step 3: Subtract that amount from the maximum deduction

Example: Single filer with $90,000 MAGI

Excess: $90,000 minus $75,000 equals $15,000

Reduction: $15,000 multiplied by 0.06 equals $900

Deduction: $6,000 minus $900 equals $5,100

Example: Joint filers with $200,000 MAGI

Excess: $200,000 minus $150,000 equals $50,000

Reduction: $50,000 multiplied by 0.06 equals $3,000

Deduction: $12,000 minus $3,000 equals $9,000

Once MAGI hits $175,000 (single) or $250,000 (joint), the deduction drops to zero.

How the Deduction Reduces Your Tax Bill

So, how does the senior deduction work in practice? It is an above-the-line adjustment to income that reduces your taxable income, not your tax liability directly.

Direct Impact on Taxable Income

The $6,000 deduction (or reduced amount) is subtracted from your income after AGI is calculated, lowering the amount subject to federal income tax.

Example: Single filer, age 67, $80,000 income

Without deduction: Taxable income equals $80,000 minus $15,750 (standard) minus $2,000 (age add-on) equals $62,250

With senior deduction: $80,000 minus $15,750 minus $2,000 minus $6,000 equals $56,250

Savings: $6,000 multiplied by 22% tax bracket equals $1,320 tax reduction

Even a partial deduction can save hundreds. The average middle-income senior is expected to save $220 to $300 annually.

Bracket Protection and Refund Boost

By reducing taxable income, the deduction can keep you in a lower tax bracket, increase your tax refund, and reduce exposure to Medicare IRMAA surcharges if income stays below $97,000 single or $194,000 joint.

However, be cautious. Large withdrawals from IRAs could push you into the phase-out range, reducing or eliminating the deduction.

Claiming the Senior Deduction: Step-by-Step

You cannot just check a box. Here is how to claim the deduction correctly.

Required Form: Schedule 1-A

The IRS introduced Form 1040 Schedule 1-A, Enhanced Senior Tax Deduction, to claim the benefit. You must complete Schedule 1-A and attach it to your Form 1040 or 1040-SR. Enter the deduction amount on the main form.

No proof of age is required with the return, but keep records such as birth certificate or passport in case of audit.

SSN Requirement

You must provide the Social Security number of each qualifying individual. For married couples, both SSNs are required.

When to File

The deduction is first available for 2025 tax returns, filed in 2026. It applies to tax years 2025, 2026, 2027, and 2028. Returns filed in 2029 will be the last to claim it for 2028 income.

How It Stacks With Other Senior Tax Breaks

One of the most powerful aspects of how the senior deduction works is that it adds to, not replaces, other senior tax benefits.

Total Deduction Potential (2025)

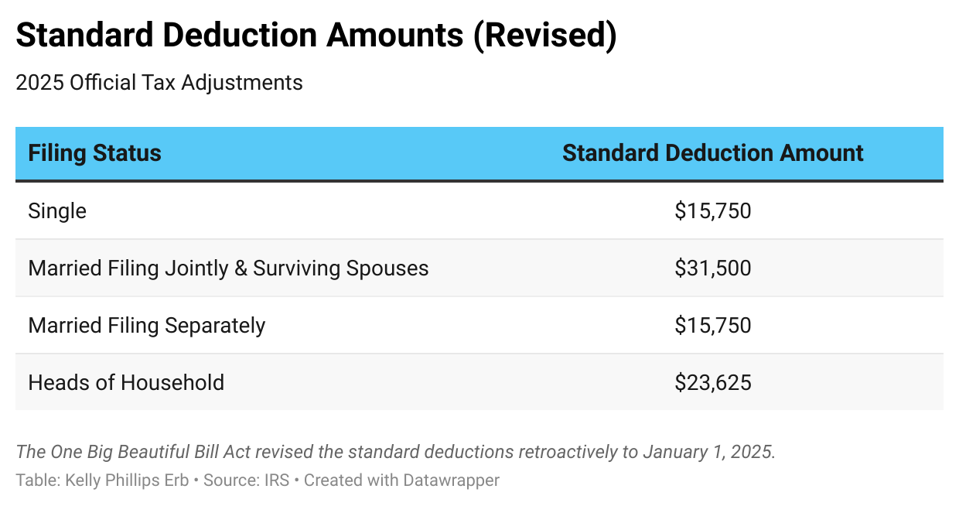

For single filers: Base standard deduction of $15,750 plus $2,000 age add-on plus $6,000 senior deduction equals $23,750 total.

For head of household: Base standard deduction of $23,625 plus $2,000 age add-on plus $6,000 senior deduction equals $31,625 total.

For married filing jointly (both 65 or older): Base standard deduction of $31,500 plus $3,200 age add-on plus $12,000 senior deduction equals $46,700 total.

The key difference is that the $2,000 age add-on is only available if you take the standard deduction. But the $6,000 senior deduction is available even if you itemize.

Itemizing vs. Standard Deduction: Which Wins?

Seniors should compare both paths. Itemizers add the $6,000 deduction to their Schedule A total and see if it beats the enhanced standard deduction. Standard filers combine base, age add-on, and senior deduction for maximum benefit.

Pro tip: If your medical expenses, SALT, or charitable contributions exceed the total standard deduction, itemizing may still win, even with the senior deduction.

Who Benefits Most and Who Does Not

Despite its broad eligibility, fewer than half of seniors will benefit from this deduction.

High-Benefit Groups

Middle-income seniors benefit most because their MAGI is below the phase-out threshold and they have taxable income high enough to owe tax. Upper-middle-income couples can claim the full $12,000 deduction before phase-out hits. Seniors doing Roth conversions can use the deduction to offset conversion income, allowing larger tax-free transfers.

Example: A married couple, both 67, with $180,000 MAGI.

Phase-out reduction: $30,000 multiplied by 0.06 equals $1,800

Deduction: $12,000 minus $1,800 equals $10,200

Tax savings: $10,200 multiplied by 22% equals $2,244

Low- or No-Benefit Groups

Low-income seniors do not benefit because their taxable income is below the standard deduction and they owe no tax to offset. Top 20% earners do not benefit because their MAGI exceeds $250,000 (joint) or $175,000 (single), so the deduction is fully phased out. Married filing separately filers are ineligible regardless of income or age.

According to the Tax Policy Center, 77% of total benefits go to middle- and upper-middle-income households. Low-income seniors, who may need relief most, often see no benefit because they owe little or no tax.

Strategic Uses in Retirement Planning

Smart planning can maximize the value of the senior deduction, especially since it is only available for four years.

Time Income to 2025-2028

Because the deduction expires after 2028, consider bunching income into these years. Delay IRA withdrawals until 2025. Realize capital gains before 2029. Accelerate pension or annuity payments. This strategy increases deductions when they are most valuable.

Roth IRA Conversions: A Perfect Pair

The senior deduction can offset income from Roth conversions, making them more tax-efficient.

Example: Convert $20,000 from a traditional IRA in 2026.

Without deduction: $20,000 taxed at 22% equals $4,400 tax

With $6,000 deduction: $14,000 taxed equals $3,080 tax

Savings: $1,320

But caution: The conversion increases MAGI, which could trigger the phase-out. Always run projections before proceeding.

Expert tip: Convert just enough to stay below the phase-out threshold ($75,000 single or $150,000 joint) and maximize the deduction.

Frequently Asked Questions About the Senior Deduction

Do I need Social Security to qualify?

No. You do not need to receive Social Security. Age, filing status, and MAGI are the only requirements.

I am 62 and collecting benefits. Am I eligible?

No. You must be 65 or older by year-end, regardless of when you started Social Security.

I am 69 but not collecting Social Security. Can I claim it?

Yes. Age is the only requirement. Receipt of benefits does not matter.

What if I turn 65 in December?

You qualify for the full deduction (subject to income limits) as long as you are 65 by December 31.

Does this replace the extra standard deduction?

No. You can claim both. The $2,000 additional standard deduction is available if you take the standard deduction. The $6,000 enhanced senior deduction is available regardless of whether you itemize.

Can I claim it if I itemize?

Yes. This is a key advantage. The $6,000 deduction is available whether you itemize or take the standard deduction.

What happens after 2028?

The deduction expires after tax year 2028. Any extension requires new legislation. Given the $90.8 billion cost over four years, future renewal is uncertain.

Key Takeaways for Using the Senior Deduction

The enhanced senior tax deduction is a valuable but temporary tax break that can save eligible seniors hundreds to over $1,000 annually. It works best for middle-income retirees under the MAGI cap, couples filing jointly where both spouses are 65 or older, taxpayers who can time income to 2025-2028, and those doing Roth conversions who want to offset income.

But it is not a universal benefit. If your income is too high or too low, you may see little or no advantage.

Action steps to take:

- Check your age and filing status. Are you 65 or older and filing jointly if married?

- Calculate your MAGI. Are you under $175,000 (single) or $250,000 (joint)?

- Compare itemizing vs. standard deduction. Which gives you the lowest tax?

- Plan income timing. Can you shift gains or withdrawals into 2025-2028?

- Consult a tax professional. This is especially important if you are near phase-out thresholds or doing conversions.

The senior deduction is a limited-time opportunity. Use it wisely, because after 2028, it may be gone for good.