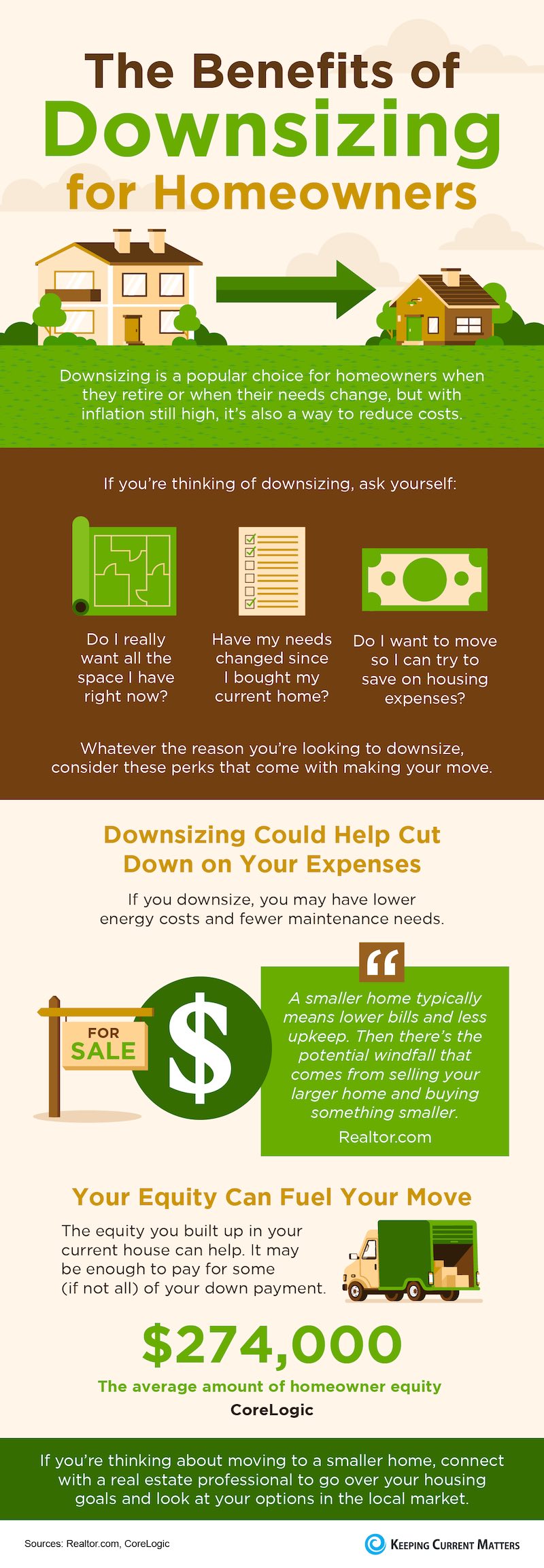

For many seniors, staying in a longtime family home feels like holding onto memories, identity, and independence. Yet as retirement progresses, that same home can become a burden, costly to maintain, difficult to navigate, and isolating from community. With 1 in 3 baby boomers saying they will never sell, the emotional pull to stay put is strong. But financial reality, shifting lifestyles, and aging bodies are pushing more seniors to ask: should I downsize?

The answer is not universal, but the data suggests now may be a strategic moment to consider it. Home equity is at record highs, $212,000 on average, and housing supply has improved, giving buyers more options. This guide breaks down the real benefits, hidden costs, emotional hurdles, and smart timing behind the decision.

Financial Benefits of Downsizing

Downsizing offers significant financial advantages for seniors, particularly those on fixed incomes. The primary benefits center on unlocking stored wealth and reducing ongoing expenses that eat into retirement budgets.

Unlock Home Equity Now

Seniors who bought homes decades ago, especially in appreciating markets, now sit on massive equity. Selling a paid-off house and moving to a smaller, lower-cost home can generate tens or hundreds of thousands in liquid cash.

You can use proceeds to:

• Fund retirement expenses without tapping investments

• Pre-pay for long-term care or health needs

• Finance travel, hobbies, or family gifts

• Create a buffer against inflation or market downturns

With the average homeowner holding $212,000 in tappable equity, now is a prime time to act.

Eliminate Your Mortgage

Over half of baby boomers own their homes free and clear. When they downsize, many can buy a new home outright, eliminating monthly mortgage payments entirely. That boost in cash flow is powerful for retirees living on Social Security, pensions, or fixed investments.

No mortgage means more predictable monthly budgets, greater flexibility during emergencies, and freedom to spend on experiences rather than bills. Even if a new mortgage is needed, downsizing often reduces the loan amount significantly.

Slash Housing-Related Costs

Big homes come with big bills. Downsizing reduces four major expenses: insurance, taxes, maintenance, and utilities.

Cut Insurance by 95%

Homeowners insurance averages $3,303 per year, but renters pay just $148. That is a $3,155 annual saving. Even if you buy a condo or townhouse, premiums are typically much lower than for single-family homes.

Lower Property Taxes

The median U.S. property tax is $3,500 per year and rising. A smaller home in a lower-tax area can cut this cost dramatically. Many states also offer tax relief programs for seniors, including freezes, deferrals, or exemptions based on age or income.

Reduce Maintenance by Thousands

Home upkeep gets more expensive and harder with age. Single-family home maintenance averages $10,593 per year, compared to $8,759 for townhomes and just $3,258 for condos. Downsizing slashes these costs and avoids the need for costly retrofits like stair lifts or walk-in showers.

Save 20–40% on Utilities

Smaller spaces use less energy. Heating, cooling, lighting, and water bills typically drop 20% to 40% after downsizing.

Hidden Costs to Watch For

While downsizing often reduces expenses, it is not universally cheaper. Certain smaller residences carry significant ongoing costs that can erode financial gains.

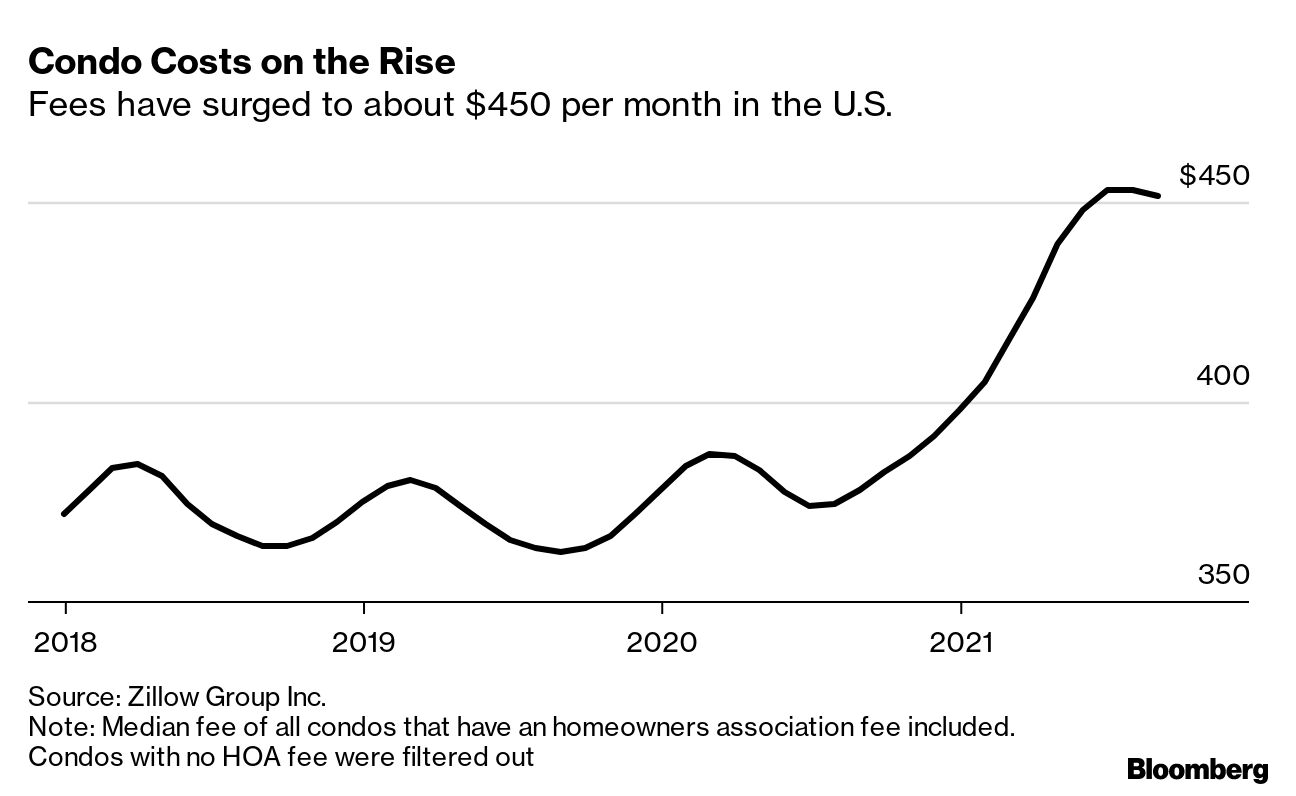

High Condo and Community Fees

Many retirees downsize to 55+ communities or condos, only to face rising monthly fees. Some CCRCs charge $1,000 to $2,000 or more per month. Fees often increase with inflation, and entry fees may be non-refundable. One woman’s $735 monthly condo fee jumped to nearly $2,000 over 15 years.

Slower Appreciation on Condos

Single-family homes tend to appreciate faster than condos. If you plan to pass wealth to heirs, this matters. Some seniors prefer to give inheritances early, sharing sale proceeds with children or grandchildren while alive.

Capital Gains Tax on Big Profits

Selling a home that has surged in value can trigger capital gains tax. There is a $250,000 exclusion for single filers and $500,000 for married couples. Gains above that are taxed at 15% to 20%.

Example: A couple sells a home bought in the 1970s for $30,000 and now worth $2.5 million. After the $500,000 exclusion, they owe tax on $2 million, potentially $300,000 to $400,000.

When Downsizing Makes Sense

Certain signs indicate it may be the right time to consider downsizing. These indicators span financial, physical, and emotional factors.

Your Home Is Too Big to Maintain

If you are hiring help for basic upkeep, you are already paying to live in a home that does not fit your needs. When routine tasks feel overwhelming, it is a sign your space has outgrown your capacity.

Red flags include avoiding repairs due to cost or effort, relying on kids or contractors for simple fixes, and feeling exhausted after cleaning or yard work.

You Are Using Less Than Half Your Space

Homes for seniors average 2,400 square feet, but only 58% is actively used. Guest rooms double as storage, dining rooms sit empty, and basements fill with clutter.

You Want to Age Safely

Falls are a leading cause of injury for seniors. One in four over 65 falls annually. Homes with stairs, bathtubs, narrow hallways, or poor lighting increase risk. Downsizing lets you choose a safer, single-level home with walk-in showers, non-slip flooring, grab bars, and better lighting.

You Are Feeling Isolated

Living far from neighbors, family, or services increases loneliness and health risks. NIH studies link social isolation to 50% higher dementia risk and 29% higher heart disease risk.

Lifestyle Gains Beyond Savings

Beyond financial benefits, downsizing can transform daily life in meaningful ways.

Reclaim 10+ Hours a Week

Residents in retirement communities report regaining 8 to 12 hours per week after downsizing. No more mowing lawns, cleaning gutters, or fixing appliances. That time becomes yours for hobbies, grandkids, travel, or rest.

Enjoy Built-In Social Life

Senior communities offer exercise classes, book clubs, game nights, lectures, and group outings. Residents report 3x more weekly social engagement than those living alone in large homes.

Simplify Your Life

Downsizing forces a natural decluttering process. You keep what is useful, beautiful, or joyful and let go of the rest. Many say they feel lighter, freer, and more in control after moving.

Emotional Challenges and How to Overcome Them

Leaving a longtime home is often emotionally difficult. Understanding these challenges helps you prepare and navigate them successfully.

Letting Go of Memories

Your home holds decades of milestones. Leaving it can feel like losing a part of your identity. But memories are not in walls, they are in you. You take them with you.

Pro tip: Take photos of meaningful spaces before you go. Create a digital album to share with family.

Decluttering Without Regret

Sorting through a lifetime of belongings is hard. Avoid a maybe pile. If you are not sure, let it go. Use labeled bins for keep, donate, and discard. Enlist help from family or a senior move manager to stay objective.

Share Heirlooms Before You Go

Give meaningful items to loved ones now. Let your granddaughter pick her favorite teacup. Let your son have your tools. This prevents posthumous disputes and strengthens bonds.

Best Time to Downsize

Experts agree: the best time to downsize is before it becomes a necessity. When you move proactively, you choose your destination, control the timeline, and avoid rushed decisions during a health crisis.

Ideal Timeline: 6–18 Months Ahead

Start planning at least six months before you want to move. This gives you time to visit communities, sort belongings, hire help, coordinate movers, and transfer utilities. Rushing leads to mistakes.

How to Plan Your Move

Successful downsizing requires thoughtful preparation. Follow this framework for a smoother transition.

Pick Your Destination First

Your new home’s size and layout should guide what you keep. Options include condos, townhomes, 55+ active adult communities, assisted living, CCRCs, or co-housing with family.

Try before you buy: Stay 2 to 3 days in a community to test the vibe, food, and accessibility.

Use the Room-by-Room Method

Get a floor plan of your new home. Map out where furniture will go. Eliminate duplicates, extra dishes, or décor. Save sentimental items for last.

Digitize Everything Important

Turn photo albums, slides, VHS tapes, and letters into digital files. Store them on encrypted drives or cloud services. Share with family via USB or secure links.

Label Boxes Smartly

Label each box with the room, contents, and box number. Number boxes after packing all of them so you do not have to renumber later.

Pack an Essentials Bag

Bring a separate bag with medications, toiletries, 2 to 3 days of clothes, ID, insurance cards, legal docs, chargers, glasses, and a favorite blanket or photo.

Support Services to Hire

Professional help makes downsizing significantly easier. Several types of specialists exist to assist with different aspects of the transition.

Senior Move Managers

These specialists help older adults transition homes. Services include decluttering, coordinating movers, setting up your new place, and managing donations or estate sales.

Search senior move manager near me for local help.

Other Helpful Professionals

Photo digitization companies, estate sale organizers, junk removal services, and senior-focused interior designers can all ease the burden.

Alternatives to Downsizing

If traditional downsizing does not feel right, alternatives exist that can improve your situation without relocating.

Age in Place with Smart Upgrades

If you love your home, consider modifying it instead of leaving. Install walk-in showers, add a first-floor bedroom, widen doorways, or put in a stair lift.

But weigh the cost. Retrofits can total $20,000 to $100,000 or more, and they do not reduce taxes, insurance, or yard work.

Choose a CCRC for Long-Term Security

CCRCs offer a full care continuum: independent living, assisted living, and skilled nursing. You move in while healthy and stay even if your needs change. Some contracts lock in fees so costs do not rise when care levels increase.

Key Questions to Decide

Answer these five areas honestly to determine if downsizing is right for you.

1. Financially, Does It Make Sense?

Consider whether your mortgage is paid off, if taxes or repairs are becoming unaffordable, and whether selling would free up cash for retirement.

2. Lifestyle: Do You Need All That Space?

Think about how often you use guest rooms, whether you entertain frequently, and if community activities would improve your life.

3. Health and Mobility

Assess whether you can safely climb stairs, if you use a mobility aid, and whether a single-level home would reduce fall risk.

4. Emotional Readiness

Reflect on whether you are attached to the house, ready to declutter, and if downsizing feels like loss or freedom.

5. Proximity to Family

Consider whether moving would bring you closer to kids or grandkids, or whether it would isolate you.

Final Verdict: Should Seniors Downsize?

Yes, if it improves your quality of life.

Downsizing makes sense when you have high equity and rising costs, want less maintenance and better safety, and are ready to simplify and embrace a new chapter.

It may not be right if you are emotionally tied to your home, do not need the money, or your house is already accessible and low-maintenance.

Strategic Takeaway

With record equity, cooling prices, and more buyer power, now may be a rare window to downsize with financial advantage. But do not rush. Talk to a financial advisor, real estate agent, and family. Weigh your needs. Plan ahead.

Frequently Asked Questions About Seniors Downsizing

What is the average savings from downsizing?

Savings vary by situation, but homeowners can save over $3,150 annually on insurance alone, plus thousands on property taxes, maintenance, and utilities. Total annual savings often reach $10,000 or more.

How do I know if I am ready to downsize?

Signs include overwhelming maintenance costs, using less than half your space, mobility challenges, feeling isolated, or wanting to unlock home equity for retirement.

What are the hidden costs of downsizing?

Hidden costs include condo and community fees that can reach $2,000 monthly, capital gains tax on large profits, and potentially slower property appreciation compared to single-family homes.

Can I avoid capital gains tax when downsizing?

Yes, you can exclude $250,000 in gains as a single filer or $500,000 as a married couple. Gains above these thresholds are taxed, but careful planning can minimize liability.

What is the best age to downsize?

There is no universal best age, but experts recommend downsizing before it becomes a necessity. Many seniors consider it between ages 65 and 75, when they are still active enough to manage a move.

Should I rent instead of buy when downsizing?

Renting eliminates property maintenance responsibilities and provides financial predictability. However, renting means no equity building and potential rent increases. The right choice depends on your financial goals and lifestyle preferences.

Key Takeaways for Seniors Considering Downsizing

The decision to downsize is deeply personal and depends on financial readiness, physical capabilities, emotional preparedness, and lifestyle goals. Current market conditions present a strategic opportunity, with record home equity and improved housing inventory giving seniors more options than in recent years.

The financial benefits are substantial, including unlocking tens of thousands in equity, eliminating mortgage payments, and reducing ongoing costs for insurance, taxes, maintenance, and utilities. However, hidden costs like rising community fees and potential capital gains tax require careful consideration.

Beyond finances, downsizing offers lifestyle improvements: more time free from home maintenance, built-in social opportunities, and safer, more accessible living spaces. The emotional challenges of leaving a longtime home are real but manageable with proper preparation and support.

The best time to downsize is before it becomes a necessity. Start planning 6 to 18 months ahead, use professional services like senior move managers, and involve family in the process. Whether you choose a smaller home, a 55+ community, or decide to age in place with modifications, the goal is the same: designing a retirement that is freer, safer, and more fulfilling.