You’ve received your first AARP membership offer at 50, started claiming Social Security at 62, and now you’re approaching 65. At what point does the law, healthcare systems, and society actually consider you a senior? The surprising answer is that there’s no single age that defines senior status. Instead, the age at which someone becomes a senior ranges from 50 to 85, depending on whether you’re talking about government programs, retail discounts, housing options, or medical classifications.

This guide breaks down every major age threshold that determines senior status, from Medicare eligibility at 65 to senior housing at 55, federal programs at 60, and retail discounts starting at 50. Understanding these distinctions helps you plan for retirement, access the right benefits, and make informed decisions about healthcare, housing, and financial planning.

The Simple Answer: There’s No Universal Senior Age

The term “senior citizen” has no single legal definition in the United States. Different organizations, government agencies, and businesses set their own age thresholds based on their specific goals and eligibility requirements. This means the answer to “when are people considered seniors” depends entirely on context.

Age 65 emerges as the most widely recognized benchmark because it marks Medicare eligibility, but this is just one piece of a complex puzzle. Some programs recognize seniors at age 50, while others don’t classify someone as elderly until 85. The variation exists because each program addresses different needs, from early retirement planning to late-life care requirements.

This multi-threshold system actually benefits consumers. It allows individuals to access senior-specific resources at different life stages, depending on their health, financial situation, and personal circumstances.

Key Age Milestones for Senior Benefits

Several specific ages mark important transitions into senior status across different domains. Understanding these milestones helps you know when to expect access to various benefits and services.

Age 50: First Access to Senior Benefits

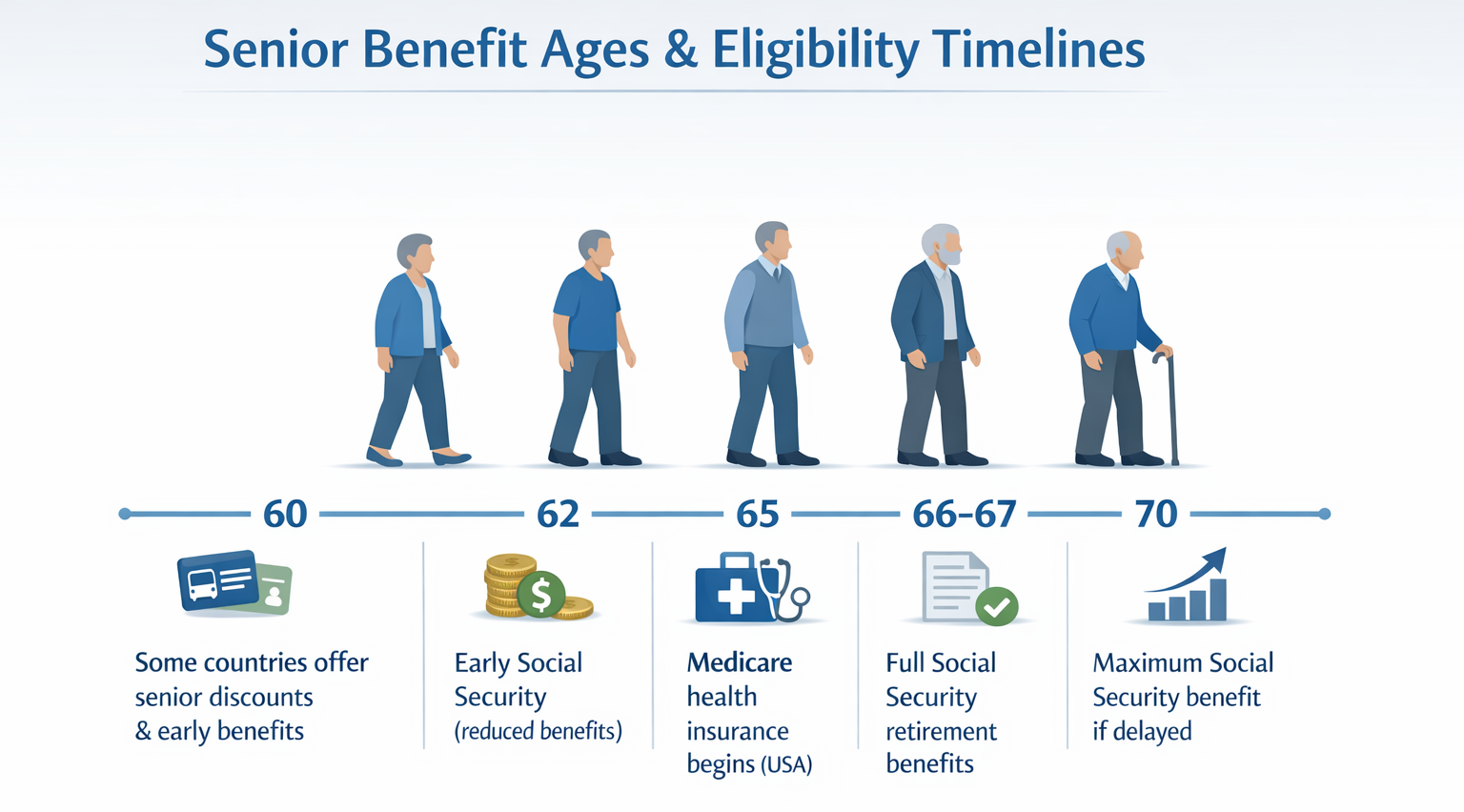

Turning 50 opens doors to your first senior benefits, primarily through AARP membership. While not a legal designation, AARP membership provides access to travel discounts, insurance rates, prescription savings programs, and advocacy efforts. Many retailers like CVS, Walgreens, and Kohl’s offer 50-plus discount programs, making this a practical threshold for early senior planning.

Age 55: Senior Housing Eligibility

The Housing for Older Persons Act (HOPA) allows communities to restrict residency to adults aged 55 and older. These active adult neighborhoods require at least 80% of units to have at least one resident aged 55 or older. They provide maintenance-free living with amenities like fitness centers and social clubs, designed for independent, active adults rather than those needing medical care.

Age 60: Federal Support Programs

The Older Americans Act sets 60 as the threshold for federally funded senior services. This includes Meals on Wheels, transportation assistance to medical appointments, caregiver support, legal aid, and elder abuse prevention services. Administered through Area Agencies on Aging, these programs help seniors remain independent often years before Medicare eligibility begins.

Age 62: Early Social Security Access

At 62, you can claim reduced Social Security retirement benefits. However, benefits are permanently reduced by up to 30% depending on your Full Retirement Age. For those born in 1960 or later, Full Retirement Age is 67. While this is an important financial milestone, it doesn’t confer broad senior status since Medicare doesn’t begin until 65.

Medicare and Government Definitions at Age 65

Age 65 represents the gold standard for senior classification in the United States, primarily because it marks eligibility for Medicare, the federal health insurance program for seniors.

Medicare Eligibility Requirements

To qualify for Medicare at 65, you must be a U.S. citizen or permanent resident who has paid into Social Security for at least 40 quarters (10 years). Medicare includes Part A (hospital insurance, usually premium-free), Part B (outpatient care with monthly premiums), Part C (Medicare Advantage private plans), and Part D (prescription drug coverage).

Your Initial Enrollment Period starts three months before your 65th birthday and extends three months after. Missing this window leads to late penalties and coverage gaps, making timing critical for new enrollees.

Social Security and Census Definitions

The Social Security Administration classifies individuals 65 and older as “elderly” for statistical and policy purposes, affecting demographic reporting and benefit forecasting. The U.S. Census Bureau similarly defines seniors as 65 and older, further subdividing this group into young-old (65-74), middle-old (75-84), and oldest-old (85+). These categories drive decisions on healthcare infrastructure, social services, and economic planning.

Senior Discounts: When Do Retailers and Restaurants Offer Savings?

Commercial senior discounts vary widely, with different businesses setting their own age requirements based on marketing strategies and profit margins.

Common Retail and Restaurant Thresholds

Many grocery stores and pharmacies set senior discounts at 55 or 60, while sit-down restaurants like Denny’s and IHOP typically require 65. Rental car companies and cruise lines often require 65, though some accept 50 with AARP membership. National park passes offer senior pricing at 62, while many museums and movie theaters reduce admission at 60.

These discounts typically range from 5% to 15%, with some offering fixed-price menus or bundled deals. AARP membership (available at 50) provides access to exclusive discounts across travel, technology, vehicle rentals, and more, even at ages when many businesses don’t otherwise offer senior rates.

Medical and Functional Classifications of Aging

Healthcare professionals increasingly assess aging based on functional status rather than chronological age, recognizing that health and independence vary widely among individuals of the same age.

The Four Stages of Senior Care Needs

The first stage involves independence, typically spanning 60 to 70, where individuals manage daily activities without assistance. The second stage, interdependence in the 70s and 80s, involves needing help with chores, medication management, or transportation. The third stage, dependency, requires regular personal care due to chronic illness or cognitive decline. The fourth stage involves end-of-life care, typically in the 80s and beyond, requiring 24-hour supervision.

These stages are not strictly age-dependent. A healthy 75-year-old may need less support than a 62-year-old with heart failure, which is why functional assessments matter more than birthdays when planning care.

Geriatric Age Subgroups

The National Institute on Aging uses 65 as the research standard but breaks it down further. The young-old (65-74) often face early aging changes like hearing loss affecting one in three individuals, vision changes, and slower metabolism. The middle-old (75-84) experience higher rates of chronic illness, with half facing significant hearing loss. The oldest-old (85+) represent the fastest-growing demographic with the highest rates of dementia, falls, and heart disease.

Cultural Perceptions: When Do People Actually Feel Old?

Self-perception of aging differs significantly from official definitions. A Psychology and Aging study found that people today believe old age begins around 74, considerably later than previous generations. Younger adults may perceive old as early as 50, influenced by marketing and cultural stereotypes.

Many people don’t identify as seniors until their 70s, even when qualifying for Medicare at 65. This phenomenon, called subjective age displacement, means that as people age, their threshold for what they consider old increases. Public figures like Jane Seymour and Helen Mirren exemplify a cultural shift toward viewing later life as a time of vitality and purpose, challenging negative aging stereotypes.

State and Local Variations in Senior Programs

State and municipal governments set their own age thresholds for senior-specific benefits, often differing from federal standards.

Public Transit and Property Tax Programs

Cities vary widely in transit discount eligibility. New York City offers half-fare at 65+, Los Angeles at 62+, Chicago at 65+, and Washington, D.C. at 65+. Most states offer property tax relief to help seniors age in place, with thresholds ranging from 60 to 65 depending on the state. These programs often include income limits and may offer deferral options letting seniors delay payments until home sale.

Recreation and Community Programs

Community centers typically offer low-cost programs for seniors at 55 or 60, including fitness classes like yoga and water aerobics, lifelong learning courses, art workshops, and travel groups. These programs combat social isolation, a major risk factor for dementia and depression among older adults.

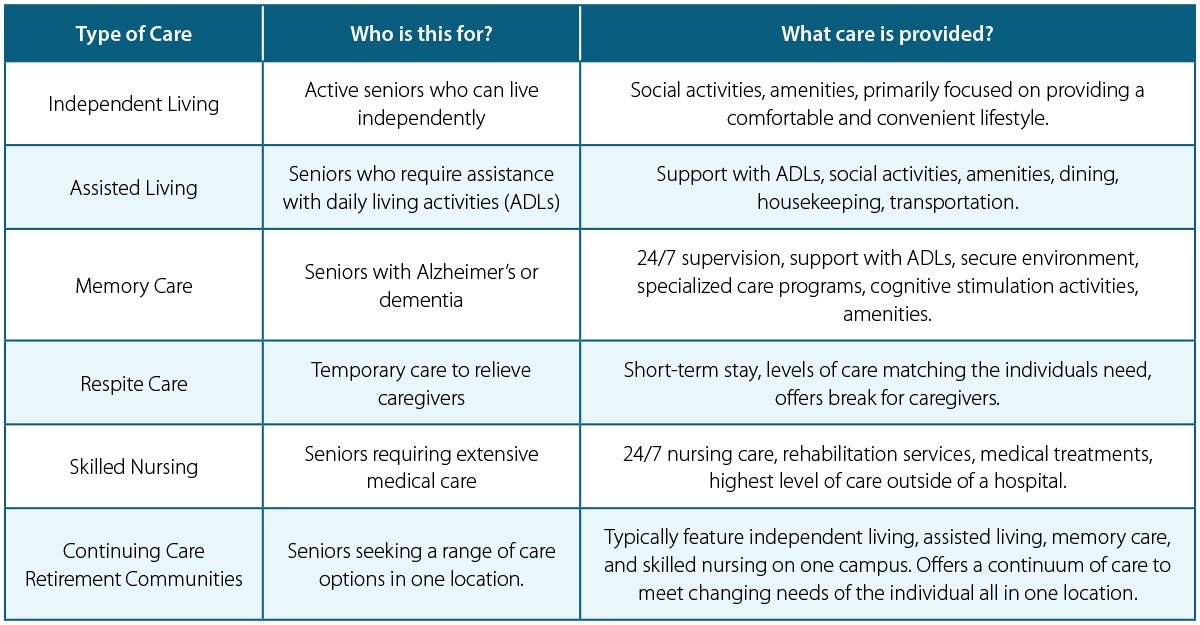

Senior Living Options by Age and Need

Housing options for seniors align more closely with functional need than specific ages, though general age ranges exist for planning purposes.

Aging in place remains the preference for 75% of seniors, requiring ability to manage activities of daily living, safe home modifications, and access to transportation. Independent living communities accept ages 55 and older for active, healthy adults seeking social connection and convenience. Assisted living typically serves those in their 70s and 80s who need help with bathing, dressing, and medication management. Nursing homes serve primarily those 75 and older, especially 85+, requiring 24-hour medical supervision.

Financial and Legal Planning for Senior Years

Strategic financial and legal planning should align with key age milestones to maximize benefits and protect your interests.

Timeline for Essential Documents and Decisions

By 50, review retirement savings and consider long-term care insurance. By 60, update wills and designate power of attorney. By 65, enroll in Medicare to avoid penalties. By 70, consider delaying Social Security for maximum benefits if you haven’t claimed already. Essential documents include power of attorney for financial decisions, living wills for medical wishes, and estate planning for asset distribution.

Frequently Asked Questions About When People Are Considered Seniors

At what age am I considered a senior for discounts?

Most retailers and restaurants consider you a senior between 50 and 65, with 55 being a common threshold. Many businesses accept AARP membership (available at 50) as qualification for senior discounts even when their stated age requirement is higher.

Does Medicare start automatically at age 65?

Medicare does not start automatically. You must actively enroll during your Initial Enrollment Period, which begins three months before your 65th birthday. Missing this window results in permanent late enrollment penalties.

Can I get Social Security benefits at age 62?

Yes, you can claim Social Security retirement benefits at 62, but they will be permanently reduced by up to 30% compared to Full Retirement Age benefits. Waiting until 67 (or 70 for maximum benefits) significantly increases your monthly payment.

When can I move into a senior housing community?

Senior housing communities under HOPA guidelines can set minimum ages of 55 or 62. These are active adult communities for independent living, not assisted living facilities which typically serve those in their 70s and 80s.

What age defines “oldest-old” for medical purposes?

The “oldest-old” category typically refers to adults 85 and older, the fastest-growing demographic in the United States. This group has the highest rates of chronic illness, dementia, and need for long-term care services.

Key Takeaways for Understanding Senior Age Definitions

Senior status is defined by multiple age thresholds rather than a single birthday, with different programs and institutions using ages ranging from 50 to 85 depending on their specific purposes. Age 65 remains the most widely recognized benchmark due to Medicare eligibility, but functional need and health status increasingly matter more than chronological age when determining appropriate care and support. Understanding these variations helps you access the right benefits at the right time, from early senior discounts at 50 to Medicare enrollment at 65 and beyond.

Rather than asking “when am I a senior,” the more practical question is “what support do I need now?” This approach leads to better planning for retirement, healthcare, housing, and long-term care regardless of which age threshold applies to your specific situation.